Non-residents can open a Wise Business account for a US LLC, but two prerequisites must be met first. Your LLC must be active, and your EIN (Employer Identification Number — the IRS-issued 9-digit federal tax ID) must be verified. As of 2026, Wise begins KYC review only after both are confirmed.

Activating US routing and account numbers costs a one-time $31 USD fee. There are no ongoing monthly subscription fees for US business profiles.

For founders based in Pakistan, Nigeria, or the Philippines, Wise is the primary US banking path. According to support.mercury.com (confirmed 2026-05-31), Mercury prohibits founders domiciled in all three countries.

Wise accepts applicants from each, though approval is not guaranteed and may require enhanced documentation. Understanding the full landscape of Bank Account options for non-resident LLC owners is essential before you begin any application.

Wise’s own signup pages never disclose the EIN requirement or country-specific restrictions. This guide fills that gap.

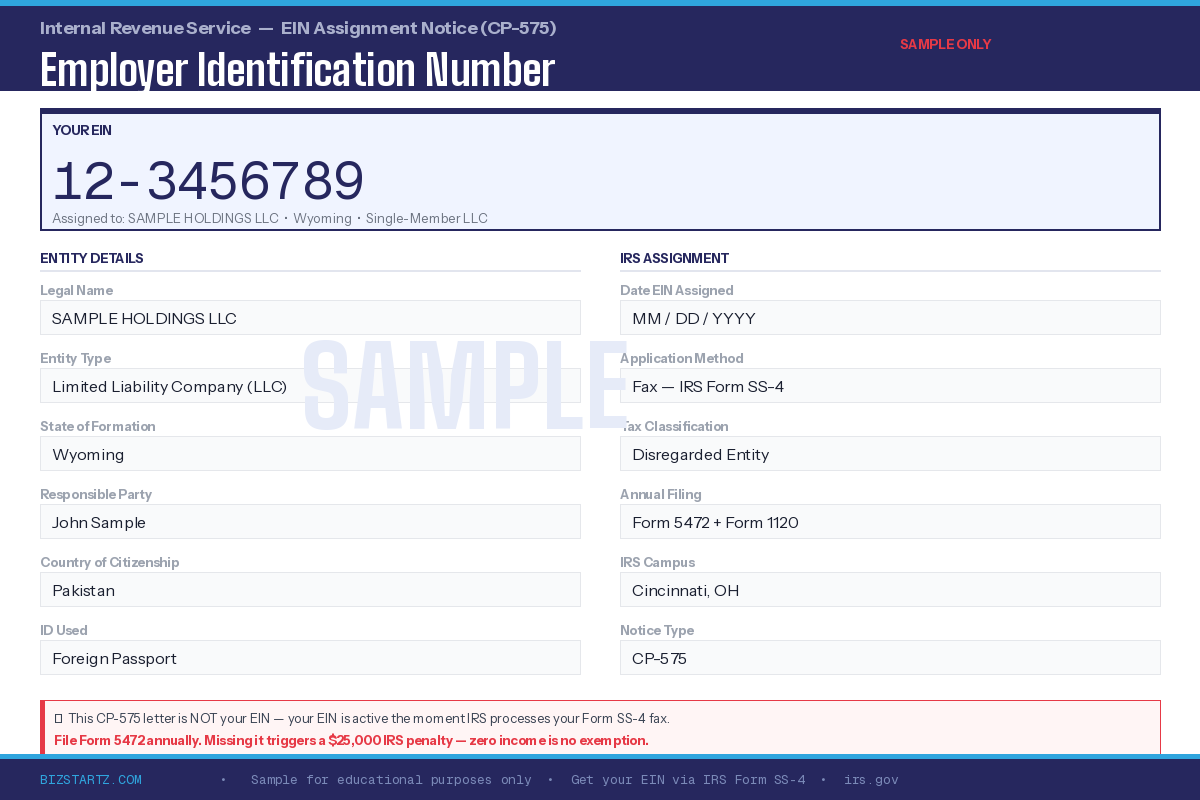

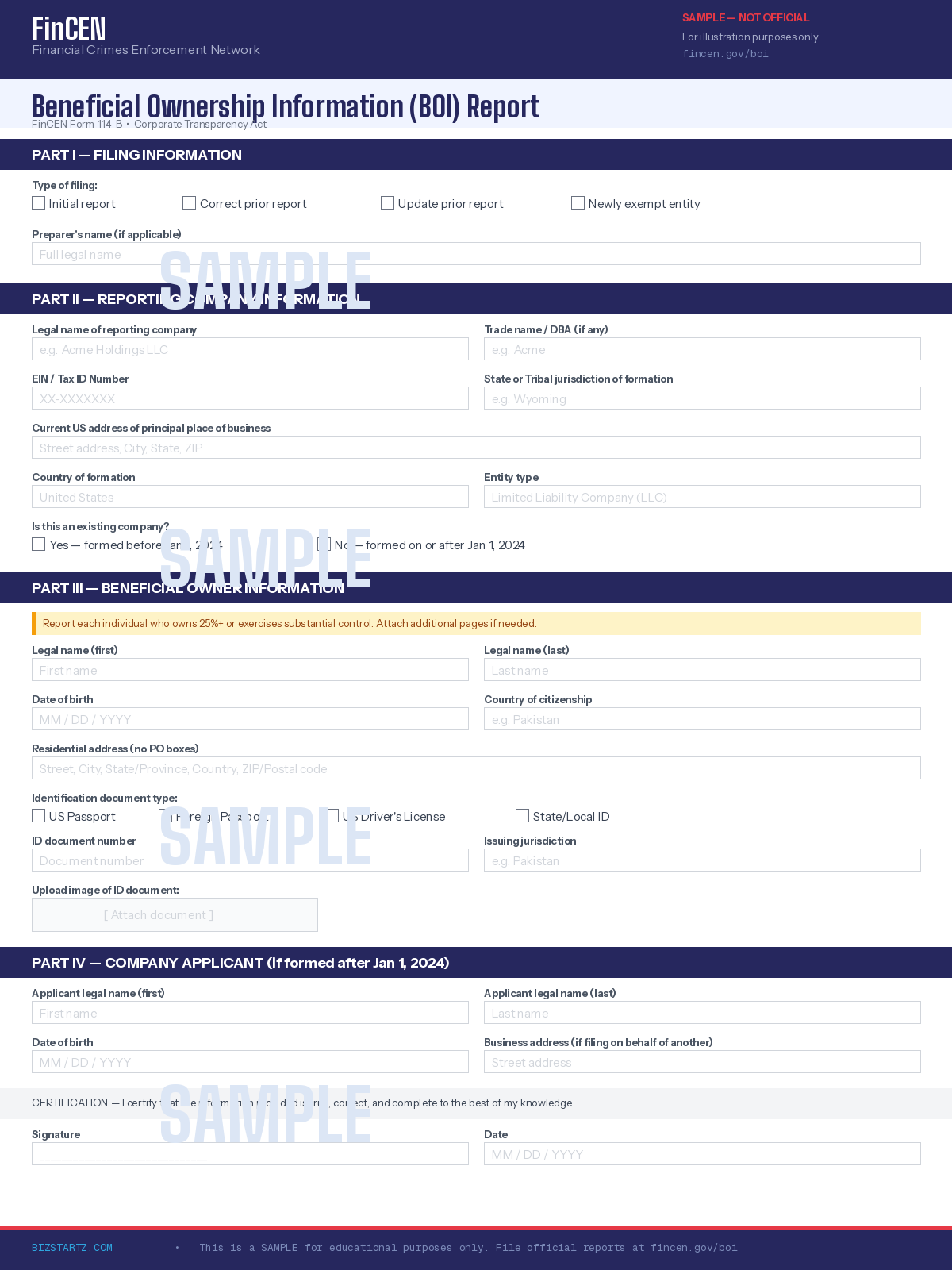

Non-residents opening a Wise Business account for a US LLC must have two documents before KYC review begins: an active LLC and a verified EIN (Employer Identification Number, the 9-digit federal tax ID issued by the IRS via Form SS-4).

According to Wise, acceptable EIN proof includes the CP575 letter, a 147C letter, or an IRS-stamped SS-4. The one-time fee to activate US routing and account numbers on Wise Business is $31 USD. There are no ongoing monthly fees for US corporate profiles.

As of 2026, Wise’s signup pages do not disclose the EIN requirement to non-residents.

Can a Non-Resident Open a Wise Business Account for a US LLC?

Yes, but only after an active US LLC and a verified EIN (Employer Identification Number) are in place. Wise Business requires both before KYC review begins.

Yes, but only after your LLC and EIN are ready

Wise Business requires both documents before KYC review begins. Wise’s signup pages do not disclose this to non-residents. Most founders discover the EIN requirement only after starting the application.

Obtaining an EIN is free directly from the IRS via Form SS-4. According to irs.gov, non-residents without an SSN or ITIN must apply by fax (approximately 4 business days with a return fax number) or by mail (approximately 4 weeks). The IRS may add delays during high-inventory periods.

Wise may also require an official IRS confirmation document the CP575, a 147C letter, or an IRS-stamped SS-4 — not just the EIN number itself.

The CP575 arrives by physical mail 2–6 weeks after EIN issuance. If you need faster proof, request a 147C by calling the IRS Business & Specialty Tax Line, the IRS faxes it to you directly.

Wise is an MSB, not a bank standard balances are not FDIC-insured

Wise is a licensed Money Services Business (MSB), not a bank. Standard account balances are NOT FDIC-insured by default. According to wise.com, FDIC pass-through insurance applies only via the opt-in Interest feature, currently provided through JPMorgan Chase N.A., and requires a US profile address plus a verified SSN or EIN.

As of 2026, the Interest feature remains entirely unavailable in New York and Alaska. Most non-resident LLC owners do not meet these conditions and will not qualify.

As of 2026, Wise Business is a licensed Money Services Business (MSB) not a bank. According to wise.com, standard Wise Business balances are NOT FDIC-insured.

FDIC pass-through insurance is available only via the opt-in Interest feature, provided through JPMorgan Chase N.A., and requires a US primary address plus a verified SSN or EIN.

The Interest feature is unavailable in New York and Alaska. Non-resident US LLC owners who lack a US address or SSN typically do not qualify for FDIC coverage through Wise.

What You Need Before Applying: LLC and EIN Sequencing

Wise Business will not approve an application without a legally formed, active US LLC. Most guides skip what must happen before you even open the Wise signup page.

Step 1: Form your US LLC

Any non-US resident can own a US LLC remotely no visit to the United States is required. Your LLC must be active and in good standing before you apply to Wise Business.

Every LLC needs a Registered Agent: a person or company with a physical street address in the state of formation. No US state accepts a PO box as a Registered Agent address.

Step 2: Obtain your EIN via Form SS-4

An EIN (Employer Identification Number the US federal business tax ID) is mandatory for Wise Business verification. As of 2026, non-residents without an SSN or ITIN cannot use the IRS online EIN tool.

Two options: fax Form SS-4 to the IRS (~4 business days with a return fax number) or mail it (~4 weeks). According to the IRS, delays can extend during high-inventory periods.

Wise Business account may require more than just your EIN number. According to Wise documentation, acceptable proof includes the CP575 letter, a 147C letter, or an IRS-stamped SS-4. The CP575 arrives by physical mail 2–6 weeks after EIN issuance.

If you need faster proof, call the IRS Business & Specialty Tax Line to request a 147C — the IRS faxes it directly to you. Founders who sell physical goods online should also check whether dropshipping requires an EIN before proceeding with their Wise application.

Step 3: Gather your Wise application documents

Prepare your LLC formation documents, EIN confirmation letter, passport, and proof of address. As of 2025–2026, Wise tightened KYC requirements for foreign-owned US LLCs. Approval is not guaranteed. Verification takes days to multiple weeks plan for this in your launch timeline.

Total time from starting LLC formation to an active Wise Business account: typically 3–8 weeks for non-residents.

Country-by-Country Eligibility: Who Can Use Wise Business with a US LLC

Eligibility varies significantly by founder country of domicile. Mercury prohibits founders from five countries outright. Wise accepts applicants from each, subject to KYC review. The breakdown below is accurate as of 2026.

India and UAE: Wise and Mercury both viable

As of 2026, Mercury does not list India or UAE as prohibited countries. Founders from both countries can apply to Mercury or Wise Business with standard KYC. Having two viable options provides flexibility apply to Mercury first for FDIC-insured deposits via Choice Financial Group and Column N.A., then use Wise Business as a backup if Mercury declines.

Pakistan: Wise is your primary path Mercury is PROHIBITED

According to Mercury’s prohibited-countries list (confirmed 2026-05-31), Mercury PROHIBITS Pakistan-domiciled founders. Wise Business accepts Pakistan-resident US LLC owners with an EIN, subject to enhanced KYC. Approval is not guaranteed.

One critical point: a Pakistan-registered personal Wise account does NOT include US routing and account numbers. Those details come only through the US LLC business profile.

Nigeria: Wise is your primary path, Mercury is PROHIBITED

According to Mercury prohibited-countries list (confirmed 2026-05-31), Mercury PROHIBITS Nigeria-domiciled founders. Wise generally accepts Nigeria-resident US LLC owners with an EIN, subject to enhanced KYC. As of 2026, address and business-evidence scrutiny for Nigerian applicants is reportedly strict.

Approval is not guaranteed, prepare strong documentation before applying.

Philippines: Wise is your strongest option, Mercury is PROHIBITED

According to Mercury’s prohibited-countries list (confirmed 2026-05-31), Mercury PROHIBITS Philippines-domiciled founders. Wise Business account accepts Philippines-resident US LLC owners with standard KYC. Wise has operated fully in the Philippines since May 2024, including local account details and a card. For Philippines founders, Wise Business is the clearest US banking path available.

OFAC-sanctioned countries and Brex

OFAC comprehensive sanctions cover Iran, Cuba, and North Korea — no US fintech can serve founders domiciled there. Syria’s comprehensive sanctions were revoked effective July 1, 2025 (EO 14312), but individual fintech policies may still restrict Syrian applicants.

According to Mercury prohibited-countries list (confirmed 2026-05-31), Nepal and Bangladesh are PROHIBITED by Mercury; Wise is the alternative path, verify current eligibility at signup.

Brex requires at least one US-based founder, so most non-resident sole owners do not qualify regardless of nationality. Nepal-based founders looking for a structured starting point can follow the steps outlined for How to Open a US Business Bank Account from Nepal before applying to Wise.

As of 2026, Mercury prohibits US LLC owners domiciled in Pakistan, Nigeria, the Philippines, Nepal, and Bangladesh from opening accounts (confirmed 2026-05-31). For founders from these five countries, Wise Business is the primary US banking path after forming a US LLC and obtaining an EIN (Employer Identification Number) from the IRS.

Wise Business account accepts applicants domiciled in all five countries subject to KYC review, though approval is not guaranteed. Pakistan and Nigeria founders face enhanced KYC scrutiny; Philippines founders face standard KYC. Brex requires at least one US-based founder and is not a realistic option for most non-resident sole owners.

What Wise Business Actually Gives You and What It Does Not

Wise provides real US banking infrastructure for non-residents, with specific costs and limitations that Wise’s own product pages do not state plainly.

What you get: US routing number, account numbers, multi-currency wallets

Activating US routing and account numbers on Wise Business costs a one-time $31 USD fee. There is no ongoing monthly subscription for US corporate profiles.

Once active, you can receive USD via ACH (electronic fund transfers) for free. According to Wise’s pricing page, receiving USD via domestic wire or SWIFT wire costs $6.11 flat per transaction, compared to the $15–30 fee traditional banks typically charge for the same transfer.

Beyond USD, Wise Business provides multi-currency wallets for holding, converting, and sending in other currencies.

What you do not get: FDIC insurance on standard balances

Wise is a licensed (Money Services Business (MSB)), not a bank. Standard Wise Business balances are safeguarded in segregated accounts but are NOT FDIC-insured.

Wise’s product page mentions FDIC coverage, but according to wise.com, that applies only via the opt-in Interest feature, which requires a US primary address and a verified SSN or EIN, and is unavailable in New York and Alaska. Most non-resident founders do not qualify.

If FDIC insurance matters to you: Mercury deposits are FDIC-insured via Choice Financial Group and Column N.A. Relay deposits are FDIC-insured via Thread Bank. However, Mercury prohibits founders domiciled in Pakistan, Nigeria, and the Philippines, making Wise Business the primary US banking path for those founders.

Stripe eligibility: it comes from your US LLC, not your bank

According to Stripe, eligibility is determined by where your business is legally registered — not your bank account or founder nationality. A US LLC is US-registered and therefore Stripe-eligible whether you bank with Wise, Mercury, or Relay.

This matters especially for founders from Pakistan, Nigeria, and the Philippines, where Stripe is unavailable or severely restricted for locally registered businesses. The US LLC is what unlocks Stripe, not the banking choice. Founders who want a step-by-step walkthrough of How to Create a US Stripe Account after their LLC and EIN are in place will find the Stripe guide covers each step once their Wise Business account is active.

Wise Business vs Mercury vs Brex: Honest Comparison

Most founders discover Mercury’s country bans or Brex’s founder requirements only after applying. The comparison below shows eligibility before you waste an application. All data confirmed as of 2026.

Comparison table: non-resident US LLC owners

| Dimension | Wise Business | Mercury | Brex |

|---|---|---|---|

| Non-resident LLC owner eligible | Yes, with EIN — subject to KYC review; approval not guaranteed | Yes, with EIN — standard KYC; approvals tightened in 2025 | Requires at least one US-based founder; most non-residents do not qualify |

| Pakistan founder | Accepted with enhanced KYC; approval not guaranteed | Prohibited (confirmed 2026-05-31) | Requires US-based founder |

| Nigeria founder | Accepted with enhanced KYC; approval not guaranteed | Prohibited (confirmed 2026-05-31) | Requires US-based founder |

| Philippines founder | Accepted with standard KYC; Wise fully operational in the Philippines since May 2024 | Prohibited (confirmed 2026-05-31) | Requires US-based founder |

| India founder | Accepted with standard KYC | Accepted; standard KYC | Requires US-based founder |

| UAE founder | Accepted with standard KYC | Accepted; standard KYC | Requires US-based founder |

| FDIC insurance | Not FDIC-insured by default; pass-through FDIC coverage only through the optional Interest feature (most non-residents are not eligible) | FDIC-insured through partner banks | Brex Cash is not a traditional FDIC-insured bank account |

| US routing & account numbers | Yes — available after one-time $31 USD activation fee | Yes — included at no additional cost | Yes — included |

| Wire receiving fee | $6.11 flat fee per domestic wire or SWIFT wire; ACH transfers are free | Varies by transaction type; check current Mercury pricing | Varies by transaction type; check current Brex pricing |

| Stripe compatibility | Yes — eligibility depends on the US LLC, not the bank account | Yes — eligibility depends on the US LLC, not the bank account | Yes — eligibility depends on the US LLC, not the bank account |

| Best for | Founders from restricted countries (Pakistan, Nigeria, Philippines) needing a US account alternative | Non-resident founders from supported countries seeking a fintech banking solution | Venture-backed startups with US presence and US-based founders |

| Monthly fee | $0 | $0 | $0 |

| EIN required | Yes | Yes | Yes |

| International transfers | Excellent multi-currency support | Supports USD-focused international banking | Available, primarily startup-focused |

For Pakistan, Nigeria, and Philippines founders: According to Mercury’s prohibited-countries list (confirmed 2026-05-31), Mercury is PROHIBITED for founders domiciled in all three countries. Wise Business is the primary path after obtaining your LLC and EIN.

For India and UAE founders: Both Wise Business and Mercury are viable. Mercury offers stronger FDIC deposit protection if approved, but Mercury declines in 2025 are often permanent.

Relay offers FDIC-insured deposits via Thread Bank. Verify non-resident eligibility directly before applying.

Common Wise Business Rejection Reasons and How to Avoid Them

Applying before your LLC is legally formed will result in an immediate rejection. Wise requires a registered, active entity not a pending one.

Applying without an EIN or official IRS confirmation document

Your EIN number alone may not satisfy Wise’s compliance review. According to Wise, an official IRS confirmation document the CP575 letter, 147C letter, or IRS-stamped SS-4 may be required during business verification.

The CP575 arrives by physical mail 2–6 weeks after EIN issuance. If you need proof faster, request a 147C from the IRS Business & Specialty Tax Line by phone, the IRS faxes it to you directly. Do not apply to Wise before you have one of these documents in hand.

Insufficient business activity evidence, especially for Pakistan and Nigeria founders

As of 2025–2026, Wise tightened KYC requirements for foreign owners of US LLCs. Applications without clear business activity evidence face higher rejection risk.

Pakistan and Nigeria founders face enhanced KYC scrutiny specifically. Approval is not guaranteed for either country. Prepare documentation before applying: an operational website, active client contracts, invoices, or digital service records. A vague business description is a common reason applications stall or fail.

Verification typically takes days to multiple weeks, same-day approval is not realistic. A rejected Wise application does not block you from applying to Relay.

However, according to Mercury prohibited-countries list, Mercury prohibits Pakistan, Nigeria, and Philippines founders entirely, regardless of application quality Wise is the primary path for founders domiciled in these countries.

Frequently Asked Questions

Can I open a Wise Business account without a US LLC?

Yes, Wise Business serves locally registered businesses in many countries. But for a US-entity account with US routing and account numbers, you need a US LLC and an EIN (Employer Identification Number — US business tax ID). Form the LLC first, then apply. Wise will ask for your LLC formation documents and EIN during verification.

Do I need an EIN to open a Wise Business account for my US LLC?

Yes. Wise requires an EIN to verify your US business. According to the IRS, non-residents without an SSN must apply via Form SS-4 by fax (~4 business days) or mail (~4 weeks). Wise may also require the CP575, 147C, or IRS-stamped SS-4 — not just the EIN number itself.

Is Wise Business FDIC-insured for non-residents?

Standard Wise Business balances are NOT FDIC-insured. According to wise.com, the Interest feature provides pass-through FDIC coverage via JPMorgan Chase N.A., but requires a US address plus SSN or EIN, and is unavailable in New York and Alaska. Most non-residents do not qualify. Mercury offers FDIC-insured deposits via Choice Financial Group and Column N.A. for eligible founders.

I am from Pakistan, can I use Wise Business for my US LLC?

Yes. Pakistan-resident owners of US LLCs with an EIN are accepted, subject to enhanced KYC. Approval is not guaranteed. According to Mercury’s prohibited-countries list (confirmed 2026-05-31), Mercury prohibits Pakistan-domiciled founders making Wise Business your primary US banking path.

I am from Nigeria, can I use Wise Business for my US LLC?

Wise generally accepts Nigeria-resident owners of US LLCs with an EIN, subject to enhanced KYC. Address and business-evidence scrutiny is reportedly strict. According to Mercury’s prohibited-countries list (confirmed 2026-05-31), Mercury prohibits Nigeria-domiciled founders, Wise Business is your primary option.

I am from the Philippines, which US banking option should I use?

Wise Business is your strongest option. According to Mercury prohibited-countries list (confirmed 2026-05-31), Mercury prohibits Philippines-domiciled founders. Philippines-resident US LLC owners are accepted with standard KYC. Wise has been fully operational in the Philippines since May 2024. You need your LLC and EIN before applying.

Does my choice of bank affect my Stripe eligibility?

No. According to Stripe, eligibility depends on where your business is legally registered — not your bank or founder nationality. A US LLC is US-registered and Stripe-eligible whether you bank with Wise Business, Mercury, or Relay. A verified EIN is required to fully activate Stripe on a US LLC account.

How much does it cost to receive USD payments into Wise Business?

ACH receiving is free. According to Wise’s pricing page, receiving USD via domestic or SWIFT wire costs a flat $6.11 per transaction. Activating US routing and account numbers requires a one-time $31 USD fee.

How long does it take to get everything ready for a Wise Business application?

EIN via fax takes approximately 4 business days. Wise KYC review takes days to multiple weeks. If Wise requires the CP575, that document arrives by mail 2–6 weeks after EIN issuance request a 147C instead for faster proof. Total timeline from LLC formation to an active Wise Business account is typically 3–8 weeks for non-residents.

What is the difference between Wise Business and Mercury for a non-resident US LLC owner?

According to Mercury, deposits are FDIC-insured via Choice Financial Group and Column N.A., but Mercury prohibits Pakistan, Nigeria, Philippines, Nepal, and Bangladesh-domiciled founders (confirmed 2026-05-31). Wise Business accepts founders from those countries, though standard balances are not FDIC-insured. Mercury approvals tightened in 2025 and declines are often permanent. Brex requires at least one US-based founder and is not realistic for most non-resident sole owners.

Conclusion

Wise Business is a viable US banking path for non-resident LLC owners,but preparation matters. Your LLC must be active and your EIN issued before you apply. Pakistan, Nigeria, and Philippines founders cannot use Mercury; Wise Business is the primary route. India and UAE founders can apply to both Wise Business and Mercury.

As of 2026, standard Wise balances are not FDIC-insured. Mercury offers FDIC coverage via partner banks for eligible founders. The Wise Business one-time US account activation fee is $31; receiving USD via wire costs $6.11 per transaction; ACH is free.

KYC approval is not guaranteed. Pakistan and Nigeria founders face enhanced scrutiny. Verification takes days to multiple weeks.

Bizstartz Pro ($299 + state fees) includes LLC formation and EIN filing via Form SS-4 so you arrive at Wise Business with every document required. Founders invoicing US clients will eventually be asked for a tax form see Form W-9 Explained in Detail to understand when a W-9 applies and when a W-8 is the correct form for non-residents instead.